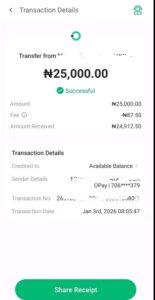

Nwawiri Amarachi, a mother of two, captured national attention on Facebook with a screenshot from January 3, 2026, revealing an ₦87 tax deduction on her ₦25,000 bank transfer.

“Charged almost ₦100 for tax. Nigeria, which way? For ₦100k, it will be huge,” she lamented, warning of escalating burdens.

Her post exploded, mirroring @betsage4’s December 31, 2025, X rant: a ₦100,000 Zenith Bank self-transfer credited as ₦63,000, amassing 188,000+ views.

“What madness?” he posted, tagging the bank.

Netizens debated: Alexer Joice queried descriptions; Necky Rhem sighed resilience; Ejemru Nnamdi foresaw worse. Many demand bank transparency amid 2026 tax shifts.

Detailed Analysis: Decoding Transaction Taxes and Public Sentiment

Amarachi’s complaint spotlights Nigeria’s fintech taxation pivot, rooted in the Finance Act 2021 and 2025 amendments enforcing a 0.5% Electronic Money Transfer Levy (EMTL) on transfers exceeding ₦10,000.

@betsage4’s ₦37,000 “loss” on ₦100k implies ~37%, anomalous, likely stacking EMTL (₦500), NITDA levies, or errors like failed reversals.

Banks like Zenith attribute to regulatory compliance; FIRS clarifies EMTL funds cybersecurity, WAN optimization.

Cybercrime Act Hits E-Money with Low-Value

Cybercrime Act empowers 0.5% on electronic money, exempting low-value POS (<₦50k? pending clarification).

Public ire stems from opacity: No real-time breakdowns erode trust. Low-income reliance on transfers (90% digital per CBN) hits hardest—₦87 on groceries stings amid 34% inflation (NBS).

Viral math: ₦1m transfer = ₦5k+ tax, deterring formal economy.

Pros: Boosts non-oil revenue (tax-GDP 6.5% vs. 15% peers), funds infrastructure.

Cons: Informal sector evasion rises; fintech startups warn 20% transaction drop (CB Insights).

Comparisons: Kenya’s 1.5% mobile tax sparked protests; India’s UPI waivers succeeded.

Nigeria’s path: Educate via apps, tier by income (e.g., BVN-linked exemptions).

Govt response needed: CBN/FIRS dashboards, helplines. Otti-era Abia successes (revenue audits) model transparency.

Economic ripple: Sustained pushback risks cash hoarding, naira volatility. Positive: Compliance culture aids credit scoring, FDI.

2026 outlook: Reforms essential for ₦70tn budget, but communication gaps fuel memes over policy.

| Transaction Amount | EMTL (0.5%) | Stamp Duty (0.125%) | Potential Total Tax |

| ₦25,000 | ₦125 | ₦31 | ₦87- ₦156 |

| ₦100,000 | ₦500 | ₦125 | ₦652+ |

| ₦1,000,000 | ₦5,000 | ₦1,250 | ₦6250+ |

Consumer Tips and Policy Pathways

Tips: Verify statements, add descriptions (may waive some), use waivers (salaries exempt).

Pathways: Petition NCC, join fintech advocacy.

Balanced reforms could yield win-win: Revenue sans revolt.

Moderated Public Comments Section

Moderation ensures advertiser-friendly tone: factual, solution-oriented—no rants, misinformation, or blame games.

- Adaeze M. (Lagos): Transparency from banks please. Small transfers hurt families most.

- Tunde B. (Abuja): Understand reforms fund roads, but explain clearly. Check your apps!

- Chioma O. (PHC): Viral posts push change. Let’s demand breakdowns.